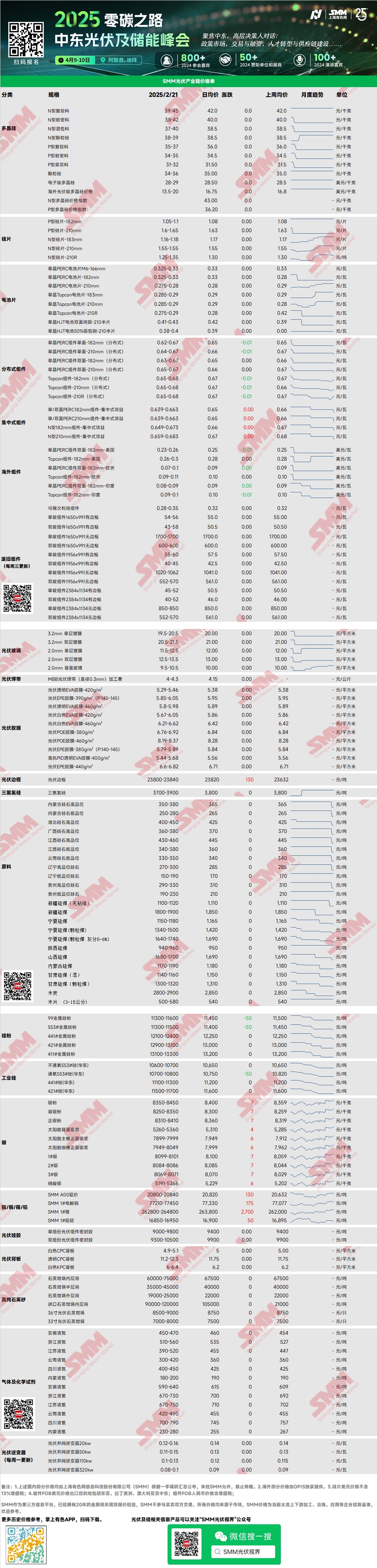

Polysilicon: This week, the mainstream transaction prices for N-type recharging polysilicon were 39-45 yuan/kg, while those for N-type dense polysilicon were 38-42 yuan/kg. The transaction range for polysilicon remained unchanged, with limited transactions in the polysilicon market this week. After a few slight transactions last week, the market gradually returned to sluggishness, and the polysilicon market temporarily stabilized. Downstream demand caused polysilicon prices to stop rising temporarily. This week, polysilicon inventory continued to increase, and some capacity may resume or commence production in the future.

Silicon Wafer: This week, domestic N-type 18Xmm silicon wafers were priced at 1.16-1.18 yuan/piece, N-type 210R wafers at 1.25-1.35 yuan/piece, and N-type 210mm wafers at 1.55 yuan/piece. The silicon wafer market continued to decline slightly this week, mainly reflected in the price reductions for 183 and 210R wafers by second- and third-tier enterprises. Overall market transactions were weak, and poor market sentiment negatively impacted prices. However, the increase in module production schedules and the rise in 210R battery prices may provide some support for silicon wafer prices in March.

Solar Cell: This week, solar cell prices showed a mixed trend. High prices for 183 and 210 cells declined, while mainstream transaction prices remained stable. In contrast, low prices for 210R cells increased, with mainstream transaction prices showing an upward trend. Mainstream prices for 183N, 210N, and 210RN cells were 0.285 yuan/W, 0.29 yuan/W, and 0.285 yuan/W, respectively. Market trading sentiment weakened this week, and the decline in 18X silicon wafer prices led to a lack of cost support for cells. Battery manufacturers faced price pressure from downstream module manufacturers. Conversely, the short-term demand for 210R cells increased, leading to undersupply and rising prices.

Module: This week, in the module market, the mainstream transaction prices for centralized PERC 182mm modules were 0.639-0.663 yuan/W, PERC 210mm modules were 0.639-0.663 yuan/W, N-type 182mm modules were 0.649-0.673 yuan/W, and N-type 210mm modules were 0.659-0.683 yuan/W. Prices stabilized, and distributed modules saw a comprehensive increase of 0.01 yuan. In February, module manufacturers produced based on demand, with production schedules down 13.88% MoM to 35GW. Module production is expected to increase in March-April, with most enterprises planning significant production schedule increases, pending confirmation next week.

End-User: From January 10 to February 16, 2025, SMM statistics showed that domestic enterprises won 17 solar module projects, with winning bid prices concentrated in the range of 0.69-0.87 yuan/W. The weighted average price for a single week was 0.69 yuan/W, down 0.01 yuan/W WoW. The total procurement capacity of winning bids was 3,207.45MW, a decrease of 8,772.04MW WoW. Domestic expectations for a rush for installations strengthened, with large-scale industrial and commercial projects filed in 2024 accelerating their installation progress. Overseas, module prices in Japan and the US remained high. In Europe, new projects were gradually launched, and distributed module prices increased by approximately 10%.

EVA Resin: This week, the mainstream transaction prices for PV-grade EVA remained at 11,100-11,500 yuan/mt, while prices for foam-grade and cable-grade EVA also rose slightly. Spot PV-grade EVA resin was in tight supply, and the impact of electricity price policies, coupled with potential rush installation activities by downstream module manufacturers, resulted in an overall undersupply in the market. Driven by both supply and demand, the overall transaction price center for EVA moved upward.

EVA Film: Prices for EVA film from top-tier enterprises remained stable this week, with mainstream transaction prices at 12,600-12,800 yuan/mt. Due to the incomplete consumption of low-cost raw material inventory from before the Chinese New Year, EVA film prices have not yet increased. However, the continuous rise in raw material prices provided cost support for EVA film price increases. Downstream demand was also robust, and EVA film prices are expected to trend upward in the future.

PV Glass: This week, PV glass quotations remained stable. As of now, the mainstream quotations for 2.0mm single-layer coated glass were 12.0 yuan/m², 3.2mm single-layer coated glass were 19.5 yuan/m², and 2.0mm back glass were 10.0 yuan/m². This week, glass transactions were limited, and top-tier glass enterprises began to refrain from selling, focusing on fulfilling previous orders. Recently, top-tier glass enterprises planned joint efforts to refrain from price cuts. On the demand side, module procurement volumes steadily increased, and the positive outlook for distributed demand significantly boosted module production schedules. Glass supply remained tight, with destocking as the main trend. Glass prices are expected to rise in the future.

High-Purity Quartz Sand: This week, domestic high-purity quartz sand prices remained stable. Current market quotations are as follows: inner-layer sand at 65,000-75,000 yuan/mt, middle-layer sand at 35,000-45,000 yuan/mt, and outer-layer sand at 19,000-25,000 yuan/mt. Prices remained stable. The domestic market atmosphere was relatively cold this week, with crucible enterprises prioritizing inventory consumption. Recently, the focus has been on negotiations for imported sand, while crucible production schedules showed limited increases. Demand was average. On the supply side, sand enterprises' operating rates rose slightly WoW, but top-tier sand enterprises maintained low operating rates, resulting in limited overall supply growth. Both supply and demand were weak, with stable prices as the priority.

Backsheet Weekly Review: This week, PV backsheet prices remained stable. The market price for white CPC backsheets with dual fluorine coatings was around 4.9-5.1 yuan/m², while transparent CPC backsheets with dual fluorine coatings were priced at 11.2-12.3 yuan/m². During the week, most backsheet manufacturers quoted higher prices, with conventional CPC backsheet quotations mostly above 5.2 yuan. However, backsheet orders were scarce, and mainstream transaction prices remained stable. The actual backsheet production in February is expected to align closely with forecasts. Due to generally poor order feedback from manufacturers during the month, the average operating rate for the backsheet industry in February is estimated to remain at a low level of 6-7%. As the end of the month approaches, backsheet orders for March may gradually be released next week. Currently, backsheet manufacturers are strongly inclined to hold firm on quotes, but whether prices can rise will depend on next week's actual order signing prices.

》View the SMM PV Industry Chain Database

![[SMM PV News] Armenia Hits 1.1 GW Solar Capacity,](https://imgqn.smm.cn/usercenter/qQwIB20251217171741.jpg)

![Spot Market and Domestic Inventory Brief Review (February 5, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)